Definition

- It refers to the manner of payment – deferred payment sale. Also known as Bai Muajjal or Bai Taqsit.

- Technically, it is a sale of commodity on deferred payment basis whether on the basis of lump sum or instalments. It applies to both musawamah and murabahah sales.

Modus Operandi

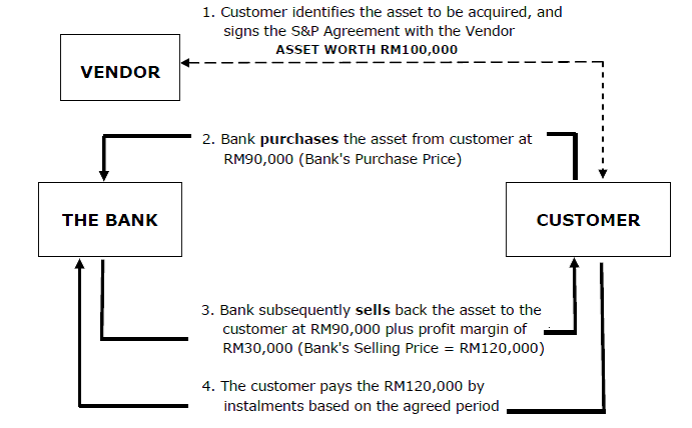

- Customer identifies the asset to be acquired, and purchase the asset by signing the S&P Agreement with the Vendor.

- The Bank then purchases the asset from Customer at RM90,000 (Bank's Purchase Price)

- Bank subsequently sells back the asset to the Customer at RM90,000 plus profit margin of RM30,000 (Bank's Selling Price = RM120,000)

- The customer pays the RM120,000 by instalments based on the agreed period

Checklist

Essential Elements

- Buyer

- Seller

- Object of Contract / Merchandise

- Price

- Contract of Offer and Acceptance (Aqad)

Necessary Conditions

Buyer & Seller

- Capable of accepting responsibilities

- Of sound mind.

- Attains the age of puberty* (matured).

- Intelligent.

- Not restricted from dealing in business transactions

-Not a bankrupt.

-Not a "safih" (an extremely extravagant person)

- Not being forced to enter into a contract

Object of Contract / Merchandise

- Must be in existence at the time of sale.

- The seller must own the object of sale and it is in his/her possession when the transaction takes place.

- The object of sale must be a property of value and of pure substance (halal).

- The delivery of the object of sale must be certain and is not by chance.

- The object of sale is known to the seller and buyer.

Price

- The price must be made known to the buyer and the type of currency is specified.

- The price must be determined and agreed by both parties.

- A deferred payment sale is allowable provided that:

-The tenor or period of payment is specified.

-The tenor would be effective from the date the object/merchandise is delivered to the buyer.

Contract of Offer and Acceptance (Aqad)

- In definite and decisive language.

- Acceptance must be consistent with the offer made by the seller.

- Offer and acceptance must be made at the one and the same meeting.

Application

- Financing a customer to purchase commodities:- houses, shop houses, land, motor vehicles, consumer goods, shares, education packages and other asset-based financing activities.

- Refinancing of assets for the purpose of redemption, construction, renovation, project financing, bridging facilities, end-financing, contract financing etc.

- BBA Securitisation.

Sources: Sources: Islamic Banking Handbook, First Edition April 2010, Institut Bank-Bank Malaysia,pp. 61-62.

No comments:

Post a Comment